The goal of this report is to explain in detail the model discussed between DAMM and Kleros during ETHCC for PNK decentralized market making on Bitfinex. We go through the different scenarios, the proposed approach, edge cases, and the reasoning behind why we arrived at this model.

The idea is to provide full transparency so the Kleros team can review and confirm they are comfortable with the model given their initial requirements.

Model — Constant-Depth Curve (CDC)

Up next is the mathematical formulation for the CD Curve. In essence, it is a function that maps the amounts to bid and ask at different price levels given a set of parameters, making it solely dependent on price, and ergo path-independent by nature. Similarly to the constant product invariant of the Uniswap protocol, this function has an invariant that represents liquidity density, which makes both a CFMM function too. However, it is in the choice of this invariant that the dynamics differ from one another: this CDC curve, unlike Uniswap, forces its liquidity depth to be constant instead of the constant product amounts, resulting in a flat liquidity pool that extends .

Notation.

State variables

- — current market price (USD per PNK).

- — LP's USD reserves at price .

- — LP's PNK token reserves at price .

- — total LP portfolio value in USD at price .

Curve parameters

- — lower price bound. At the LP holds only tokens (all USD spent).

- — upper price bound. At the LP holds only USD (all tokens sold).

- — depth scalar setting the curve's liquidity density.

Specifications

- — compliance depth requirement (USD of resting depth on each side) — 25K.

- — compliance band width (fractional distance from mid) — 2%.

Reference / derived

- — deployment reference price.

- — initial notional.

- — price at a later time ; is the price return.

A bonding curve whose USD reserves grow linearly in log-price:

with a single scalar . Compliance — providing at least USD of depth within of mid — requires

For and , the minimum is

We deploy at this floor.

The invariant preserved along any trade sequence:

By construction, USD depth within of any mid equals , uniformly across the operating range .

Path-independence

At any price , the LP's reserves are fully determined by . Two LPs arriving at the same via any sequence of market events hold identical inventory. Formally, the state map

factors through alone; no history component.

The LP is therefore a deterministic function of the venue's price. The book at any moment is the analytically specified CDC curve at the venue's current mid.

The full derivation is published separately: Constant Depth Curve — mathematical proof.

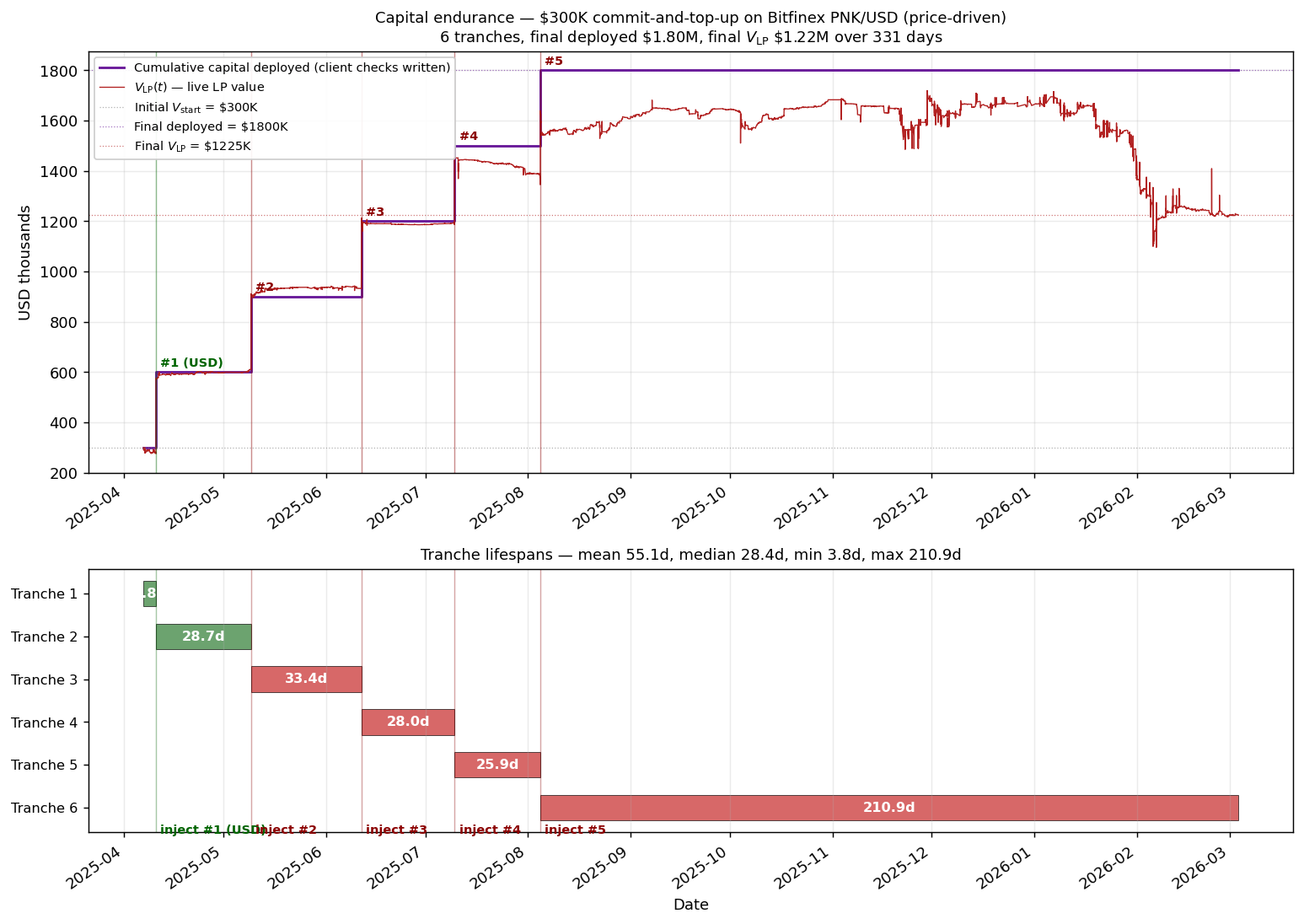

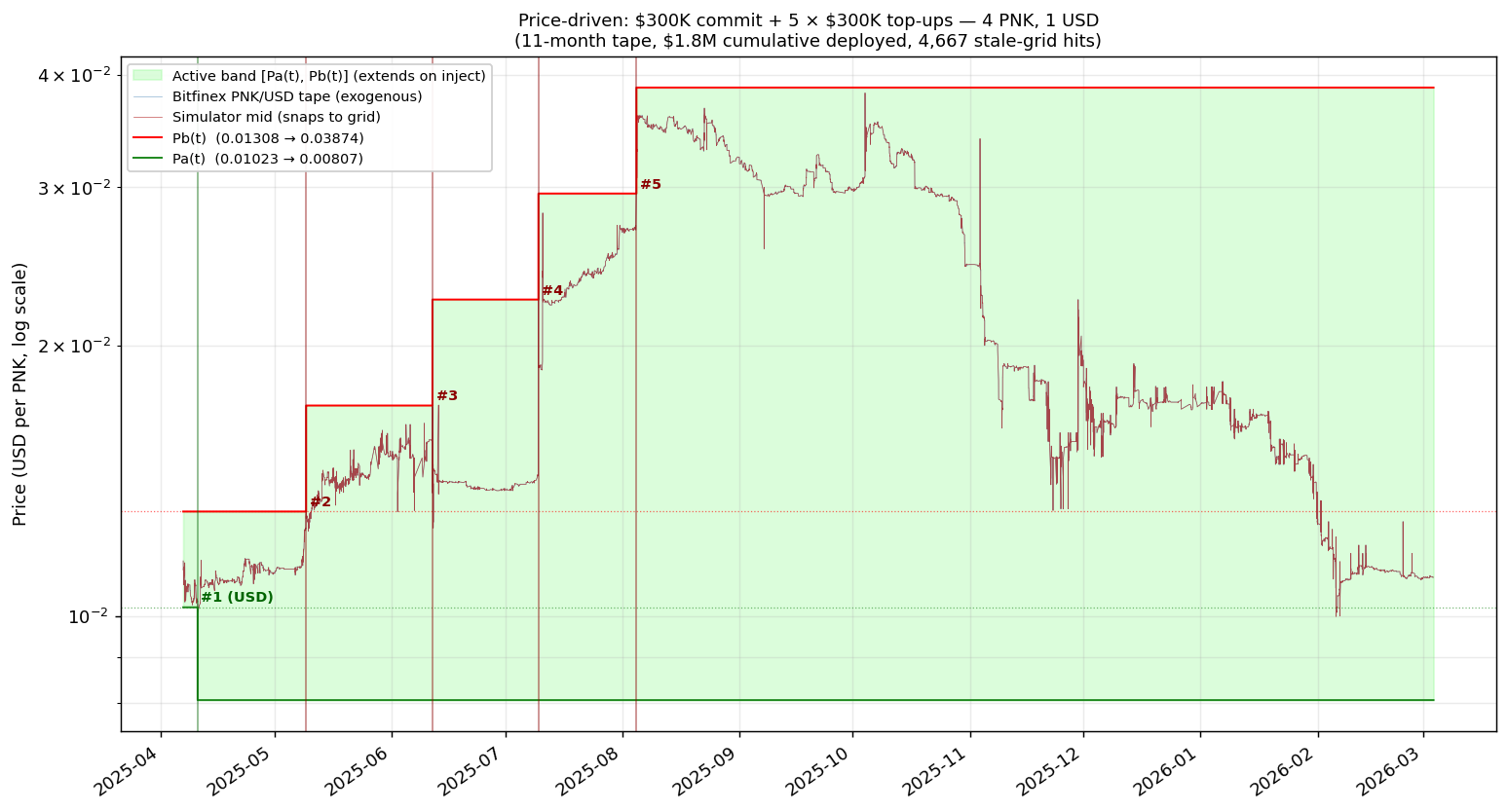

Deployment — $300K client commitment with top-up on blow-through

The client commits $300K (50% USD + 50% PNK). At this size the band is necessarily narrower than the observed 11-month price range, so boundary blow-throughs are expected and the operational model is commit-and-top-up: on an upside blow-through we inject another P_b300K in USD (extends ).

Modeling stance. Bitfinex's mid is exogenous — set by the aggregate book, not by DAMM alone. Our $300K is a small slice of the total PNK/USD liquidity; the venue's mid is dominated by everyone else, and our grid levels are filled whenever the aggregate price crosses them.

| Parameter | Value | Derivation |

|---|---|---|

| 1,262,459 | — compliance floor | |

| Initial USD on book | $150,000 | 50% of $300K commit |

| Initial PNK on book | 13,018,432 ($150,000) | 50% of P_0 = $0.01152$ |

| (initial) | 0.01023 | (−11.2% from ) |

| (initial) | 0.01308 | (+13.5% from ) |

| Top-up tranche | $300,000 | full PNK on upside / full USD on downside |

| Initial notional | $300,000 | client's posted capital |

Compliance — CP$ in the band is identical regardless of how wide the band is. Injections widen the band but do not change the depth per unit of log-distance from mid.

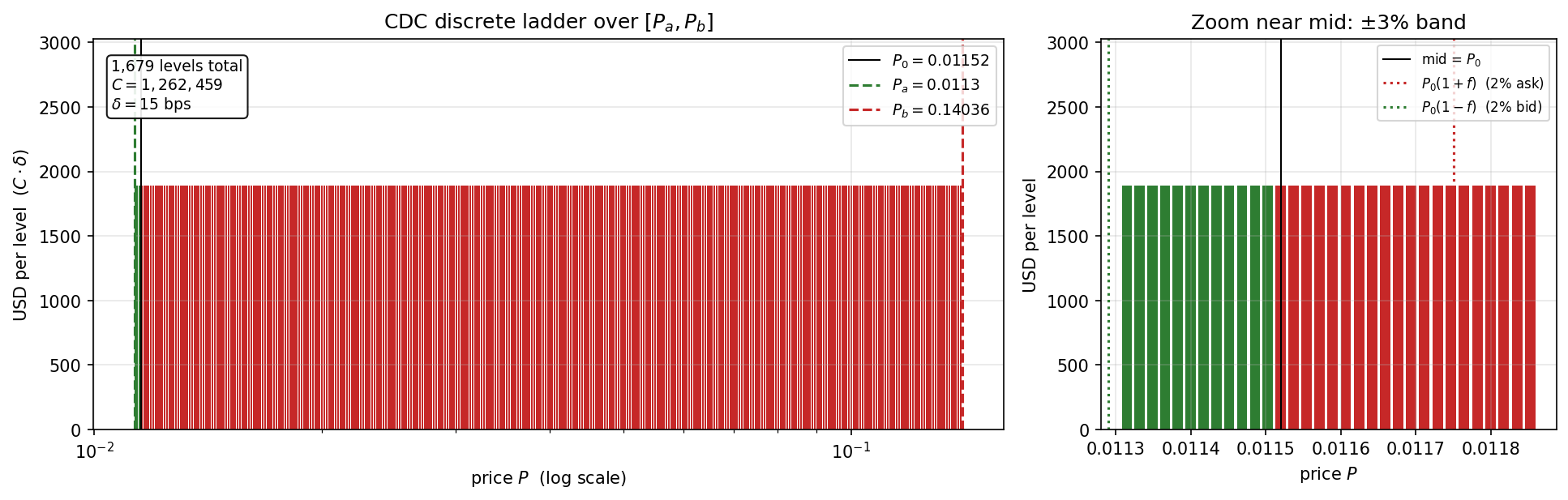

Bitfinex execution — discrete ladder, spread, and refill latency

The CDC is deployed as a discrete ladder of limit orders on Bitfinex's CLOB.

Grid. Log-uniform price levels

with half-spread spacing . The topmost bid sits at and the topmost ask at , so the bid-ask spread is

For target bps: (15 bps per side). Each level carries nominal USD (ask side: tokens; bid side: USD). Total level count over : 1,679.

Refill latency. A fill empties its level; the LP reposts after round-trip latency ms (WebSocket from a European VPS). During the level is stale. A stale-grid event fires iff a trade arrives within of the previous fill and in the opposite direction — same-direction flow walks outward into fresh levels.

Simulator. Drive the ladder with the tape's price series . On each tick, snap the target grid index to . If is above the current mid level, walk asks upward, filling each non-reposting level at its posted price and marking it reposting for ms; if below, walk bids downward analogously. Blow-through fires when the walk needs to cross or — inject $300K on the offending side, extend the band via the same closed-form CDC sizing equations, and resume. The LP state (tokens, cash) is maintained exactly; spread revenue accumulates per fill, and stale-grid hits are counted whenever a crossing intersects a still-reposting level.

Tape (2025-04-06 → 2026-03-03, 25,297 trades):

| Metric | Value |

|---|---|

| Tape price range (exogenous) | (3.8×) |

| vs initial | below — triggers 1 USD inject |

| vs inject-extended sequence | covered after the 4th PNK inject () |

| Consecutive trade pairs within ms | 10,352 (40.9%) |

Results at , initial , initial , bps, ms:

| Quantity | Value |

|---|---|

| Total blow-throughs | 5 |

| PNK injects (upside, $300K each) | 4 |

| USD injects (downside, $300K each) | 1 |

| Total capital deployed | $1,800,000 (6 tranches × $300K) |

| Final / after injects | 0.00807 / 0.03874 |

| Final | $1,224,696 |

| Fills (ask / bid) | 26,320 / 26,591 |

| Stale-grid hits | 4,667 (8.82% of fills) |

Path-independence: scope of validity. Given the coupled Bitfinex and CDC dynamics, path-independence is preserved as long as:

- Price does not fall from the range.

- Consumed orders are duly refilled before another order arrives — i.e. price can move in one direction up to the range limit, but it should not bounce back before the bid/ask is refilled.

- Grid granularity is infinitesimal.

- Spread is null.

Each violation of any of these conditions introduces path-dependent deviations proportional to the volume impacted by cumulation of each event. This is quantified over the 11-month backtest for a reference number.

Capital endurance — lifetime of one $300K tranche before the next top-up

This corresponds to the cases where the price would arrive at an edge of our position and hence the client should provide more capital, either USD or PNK, to maintain/regain path-independence.

| Metric | Value |

|---|---|

| Mean lifetime | 55.1 days |

| Median lifetime | 28.5 days |

| Min lifetime | 4.0 days (initial tranche → downside USD inject on 2025-04-10) |

| Max lifetime | 211.1 days (final tranche after inject #5, no further blow-through on the tape) |

| Time to first inject | 4.0 days (USD, downside) |

| Calendar-time average | 55.1 days / tranche |

Interpretation.

- Two-sided stress on day 4. The tape's absolute minimum of P_a = 0.01023150K USD cushion. The client must be ready to post full-USD tranches on short notice, not only PNK.

- Four PNK injects on a monthly cadence. Injects #2–#5 fire at 2025-05-09, 2025-06-11, 2025-07-09, 2025-08-04 — ~30 days apart each — as the tape climbs from 0.038.

- Seven-month quiet tail. After inject #5 on 2025-08-04 the extended covers the tape's maximum and no further boundary contacts occur for the remaining 211 days. This dominates the mean tranche lifetime of 55 days.

- Spread revenue is material. The ladder records ~53,000 fills across the tape's natural oscillations — 26,320 ask fills and 26,591 bid fills, each capturing the 30 bps spread on round trips. This is the primary revenue stream in the price-driven regime.

- Stale-grid hits are non-trivial (4,667 ≈ 8.8% of fills). These are real costs — taker flow that passed a still-reposting level and took its 15 bps of spread elsewhere. Sub-10 ms refill latency would close most of this gap.

- Path-independence of the curve is preserved between injects. Within each band the state map factors through alone. Each inject introduces a small, bounded cash adjustment at the new or (grid-quantization premium); the curve itself remains closed-form.

It is worth mentioning that Bitfinex allows insolvency for 5% of a year, roughly 18 days. This gives the maker the chance to wait for some days for markets to cool down before risking more capital.

Contingency plan. Through the monitoring services provided by DAMM Capital, both parties will be notified when price is close to an edge. An action plan must be decided for such events: either the maker can let the price fall and face insolvency for some days until the market cools down, or the client can unlock capital to extend the range. The plan is strictly situational — the 5% insolvency margin from Bitfinex is a card to be used when facing uncertainty.

Conclusion

Every parameter in this deployment is derived, not chosen:

- One free parameter. . Fixed by the contract.

- Initial band derived from client capital. and follow directly from the $300K 50/50 commit via the closed-form CDC sizing equations; no calibration.

- Top-up policy is mechanical. On boundary contact, inject P_aP_b$ from the same sizing equations. Zero discretion.

Across the 11-month tape the MM fired four $300K PNK injects (upside) and one $300K USD inject (downside), deploying $1.8M cumulative capital across six tranches with a mean 55-day tranche lifetime. The final tranche survives untouched for 211 days after inject #5. Path-independence of the curve is preserved between injects; each inject introduces a bounded and accountable cash adjustment at the new or .

Spread revenue is the primary earnings stream: ~53,000 fills across the tape's natural up-down oscillations, 30 bps captured per round trip. Stale-grid hits (4,667, ≈8.8% of fills) are real costs from taker flow passing still-reposting levels; sub-10 ms refill latency would close most of this gap. Every captured basis point of spread flows to the LP with no maker-fee leakage.

For each insolvent situation, DAMM Capital and the client must have pre-agreed action scenarios for fast reactions. If price continues deviating, extending the range for the scarce token is the sole alternative to preserve path-independence. However, there are 18 days of the year where the maker can afford insolvency — a valid alternative at the expense of losing path-independence for that time frame. Those are the sole two options when facing such events.