If you are active on Crypto Twitter, you've probably noticed that "risk-adjusted yields" are everywhere these days.

Every vault. Every ERC-4626 wrapper. Every tokenized T-Bill or PEPE-themed structured note. All of them apparently offer risk-adjusted returns.

The point of this post isn't to bash those using the term — I've been working with "risk-adjusted" frameworks since 2022 thanks to @clesaege at Kleros. The goal is just to share my take on what it actually means.

That being said… let's be honest: these days, "risk-adjusted" feels like a commodity label.

Let's break it down.

ELI5: what even is risk-adjusted?

Risk-adjusted means your strategy doesn't aim to give you the highest APR on the table, but the best tradeoff between yield and the actual risk you're taking to get there.

Simple example:

- Strategy A: You're looping a junior tranche in a delta-neutral stablecoin vault with a 90% LTV and 1.5% liquidation margin. Nominal APR = 20%.

- Strategy B: You buy a Pendle PT for tokenized T-Bills. No leverage, no volatility. Nominal APR = 11.5%.

Both sound good. But are they equally "safe"?

Obviously not.

So, risk-adjusted means asking what you're really earning per unit of risk… not just the number flashing on the UI.

APRs are (sorta) objective…

You can see APRs on-chain. You can compute them epoch by epoch. It's (mostly) tangible — especially if you denominate it in USD or ETH and ignore native-point-farming (though today it's a big part of the equation).

Just note: many APRs are inflated or misleading, either due to:

- incentives that are not really liquid (good luck dumping 200K worth of some governance token on-chain)

- under-the-table TVL deals

But we'll save that rant for IRL asados 🇦🇷🥩

RISK… vibes?

This is where things get interesting.

IMO, to actually calculate a risk-adjusted yield, you need two things:

- Expected return (somewhat objective)

- Estimated risk (pure subjectivity… or mostly at least)

Teams like @gauntlet_xyz, @SteakhouseFi, @Re7Labs and others have done a solid job building trust — mostly by staying consistent and making few mistakes.

So yeah, some of them have earned the right to say their yields are "risk-adjusted."

But here's the thing: new protocols are popping up every week — bringing novel yield-bearing assets, fresh architectures, and all kinds of incentive models and risks. We're already seeing a mix of strategies like cash & carry, on-chain private credit, and others, each with their own risk profiles and mechanics. This constant innovation creates a growing need for more asset managers — not just for crypto-native users, but especially for bringing TradFi allocators on-chain.

And ultimately, it's the asset manager who decides whether a yield is truly risk-adjusted for their LPs.

And while some risk curators are doing great work… that's not always the case. And more importantly:

A good outcome (aka not getting rekt so far) doesn't always mean it was a good decision.

Let me walk you through a quick story to show what I mean.

Against the odds: a poker tale

You're dealt a 7 and 2 (terrible hand), but you go all in anyway…

The flop and river cards give you a full house, and boom… you win big.

A bad decision (statistically one of the worst hands in poker, with very low chances of winning), but luck's on your side. But the flip side is true too: you could go all in with Aces and still lose to a lucky 7 and 2 full house.

Lucky guy.

A well-debated example was the addition of Ethena to the collateral backing of DAI/USDS, followed by Aave joining the conversation and eventually including exposure to USDe as well — at a time when Ethena was only a few months old and hadn't yet faced the kind of major stress tests we've seen more recently (like the Bybit incident and the sharp drop in funding rates).

At the core, the debate was about whether that exposure represented a positive risk-adjusted yield — and clearly, there was no real consensus at that point in time.

So why do all vaults claim to be "risk-adjusted"?

We can all agree though that USDC is a safer asset than any of the newest stablecoins, and the same applies to ETH against any other wrapper/LST…

But there's no ISO certification or objective universal benchmark to assign risk to a crypto asset (more on this later in the post).

So, how do we deal with it?

At DAMM and Kleros, when we say "risk-adjusted yield," it means we apply our internal risk framework to every strategy we evaluate.

Let's say we're looking at an Aura LP vault. To understand its real risk, we break it down:

- Aura smart contract risks (code, audits, governance, upgradability)

- Balancer smart contract stack

- Oracle feeds used for the position

- Volatility of both LP assets (we do market neutral mostly)

- TVL over time

- Risk on custody setup (if any) and opsec of respective teams — (pretty difficult to check)

- Chain-level risk (Ethereum = our risk-free base)

And you can make your own estimate framework for different protocols.

So, we can assign each a score, give it a weight, and calculate an expected risk value.

An example

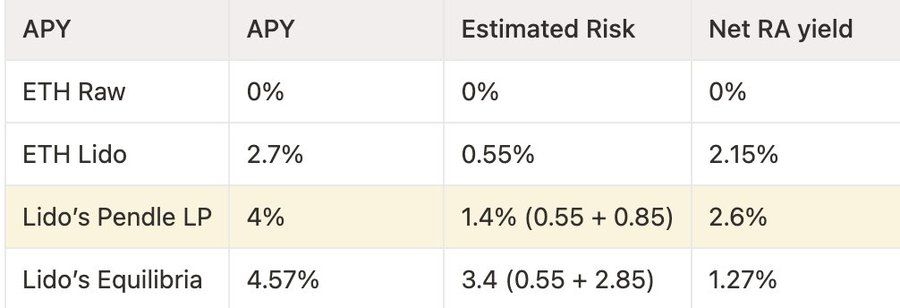

For example, let's say you're looking for ETH-denominated returns and want to compare simply holding ETH versus using Lido's wstETH on Pendle or Equilibria.

Step one. Try to estimate the risk of the strategy using whatever framework you've defined.

Step two. Then we compare that to the actual APR the strategy is offering. If it yields 12% but we estimate it carries 7% of systemic or tail risk annually… well, maybe that 12% isn't so attractive anymore.

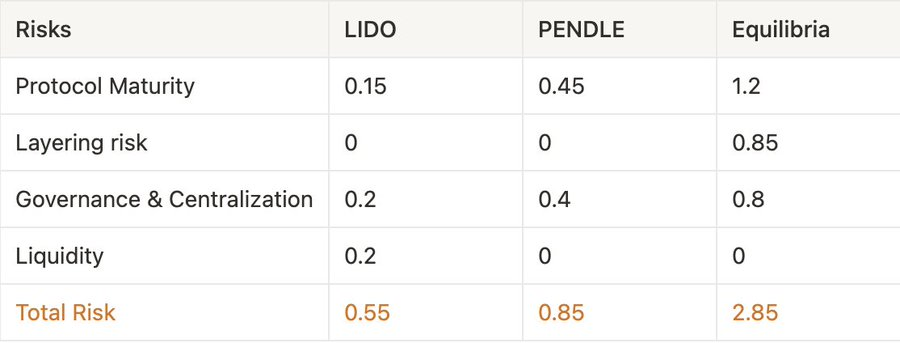

For example, let's check Lido's pool on @pendle_fi and Equilibria (Equilibria is a booster on top of Pendle, similar to Convex for Curve or Aura for Balancer).

Let's assume that you don't have Pendle max boost but you end up getting a 4% yield on Lido's Pendle pool, and you have the option to deposit that LP token on Equilibria as well to boost your PENDLE rewards.

Basically, you want to see if that extra layer of risk (these numbers are illustrative) is worth it or not, so you compare that APR (objective) vs. the estimated risk (subjective).

So… what would be the conclusion on this example?

Basically, even if the nominal APR on Equilibria is higher than just holding your LP position on Pendle, the added risk doesn't justify it. So, you go with Pendle — where the extra yield feels justified compared to simply staking in Lido.

Each asset manager or protocol might conduct a deeper or more superficial analysis (or none at all) of the underlying layering risks in each strategy to determine whether a new strategy is worth their LPs' funds. They may have a more detailed approach or a broader way of estimating risk, but in the end, some form of risk estimation is necessary and ends up being part of the due diligence process.

But isn't that… subjective?

And yeah… that's the point.

Every asset manager, DAO, or vault team has its own interpretation of risk. You can have two serious teams — one allocating to a 12% vault, another to a 4.5% — both claiming "risk-adjusted" returns.

Because maybe the first is fine with having the trust assumption of a brand new BTC derivative issuer, or they estimate that there is no possibility of drawdown events in an LST. Maybe the second prices an extremely high risk premium on the opsec setup of that same BTC wrapper team, and a small multisig threshold therefore means an extremely huge risk of losing 100% of their assets. Same asset being evaluated. Different frameworks. Different outcomes.

Others would give way more weight to immutable contracts than to a protocol with 10x more TVL but upgradeable contracts.

That's not necessarily bad. But it's important to recognize that "risk-adjusted" is not a metric. It's a lens.

But if you wanna be here in the long term, you want to make sure not to heavily misprice risk, chasing a 20% APY while having a very high chance of losing 100% of your "stablecoins."

Note: this doesn't mean a good risk manager can't face drawdowns or hacks. As mentioned before, a good decision can still lead to bad results and vice versa. But you just need to act accordingly and be able to understand different levels of risk when entering a position.

Is it possible to think of a unified risk metric?

In TradFi, you have rating agencies like Moody's, Standard & Poor's (S&P), and Fitch that price the risk of certain investments — and their ratings are often used as assessment tools by capital allocators, insurers, and others.

Crypto is still super early, and we have a very limited set of real-world scenarios to accurately price the risk of certain assets or platforms.

You could also look at the price of insurance as a proxy for how the market is pricing risk. As I outlined when introducing my design around @SafuLabs, insurance in crypto is still extremely immature — and so far, Nexus has been the only solid team with some traction.

That's why, as mentioned before, there are so many divergent takes on how risky something actually is.

And yeah, while there are definitely some shady setups out there, we also have a much higher transparency standard. I mean — how cool is it that you can actually see and verify all outstanding loans and borrows happening on-chain?

Still, having some sort of consensus between capital allocators and field experts could not only benefit crypto users but also help push institutional adoption forward.

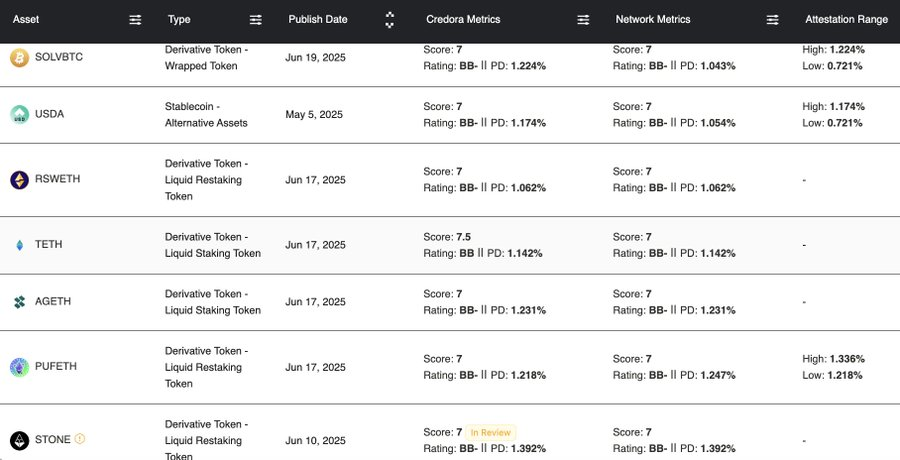

A unified approach to risk assessment would be ideal. Personally, at Kleros and DAMM, we really like the work @CredoraNetwork is doing. It allows me to price risk more accurately without having to spend as much time building a framework from scratch, while still having the chance to weight my POV and insights on that asset.

Now imagine combining that with open innovation… on-chain agents, prediction markets where people can literally trade their beliefs. We might actually move toward a much more efficient way to price risk.

What if you could launch a prediction market to price the risk of a specific asset? 👀

We've been brainstorming a few ideas around this… but I'll leave that for a future post focused on it.

TL;DR

- Nominal APR is what you see. Risk-adjusted APR is what you think you're getting after accounting for all potential rekt paths.

- Measuring risk is mostly subjective (audits, governance, code upgrades, oracles, chain-level risk, etc.)

- No two teams will weigh things the same way. And that's OK.

Conclusion

The share of the crypto market being managed by risk professionals will only keep growing… and you'll probably keep seeing plenty of "risk-adjusted yields" being cooked up out there.

In the end, one way or another, it still comes down to trusting your chef.

Originally published as a thread on X.